VARIOUS SOURCES/ARTICLES:

This week I joined Senator Tom Coburn of Oklahoma in the release of a bipartisan report on the causes of the financial crisis that pushed us into the recession that continues to afflict families in Michigan and across the country.

The report is the product of more than two years of work by the Senate Permanent Subcommittee on Investigations, which I chair. Over more than 600 pages, it demonstrates that the financial crisis was a man-made economic assault, the product of reckless risk-taking and rampant conflict of interest on the part of some big banks, mortgage companies and credit rating agencies.

What did we learn in our investigation? Conflict of interest is the common thread that runs through this whole sordid story. Our bipartisan report pulls back the curtain on shoddy, risky and deceptive practices. We showed that major financial institutions deceived their clients and the public, aided and abetted by conflicted and deferential regulators and credit rating agencies.

Washington Mutual Bank, the nation's largest thrift, issued thousand of mortgages that later failed and resulted in foreclosures that devastated neighborhoods. Executives at WaMu pursued a high-risk strategy of selling dubious and often fraudulent mortgages and pushing customers into high-risk, high-interest loans so WaMu could reap higher profits.

We showed how WaMu's main federal regulator, the Office of Thrift Supervision, knew all along about major problems with the bank's mortgages. But instead of cracking down, OTS treated WaMu with kid gloves, refusing to act on repeated warnings by its examiners and blocking efforts by other regulatory agencies to act. We also examined how credit rating agencies that were supposed to provide objective opinions about the quality of mortgage-related securities gave high ratings to toxic assets.

And we showed how investment banks such as Goldman Sachs assembled toxic securities, misled the clients they sold them to, and then profited by betting against the very same investments they had sold to their clients.

Last year, Congress passed the Dodd-Frank Act, which addresses many of the problems our investigation identified. It included a provision that Sen. Jeff Merkley of Oregon and I fought for, limiting the ability of banks to make risky investments for their own profit, and prohibiting them from betting against the same investments that they sold to clients.

Our report includes 19 new recommendations to further curb Wall Street excesses and conflicts of interest. Those recommendations, like the Dodd-Frank Act itself, will be opposed by some members of the financial industry that want to continue their risk-taking ways. I'll do all I can to make sure that federal regulators act with forcefulness and determination to fully implement the reforms we need.

Sincerely,

Carl Levin

Left, Susan Walsh/ Associated Press; Right, Mark Wilson/Getty Images

Senator Carl Levin, Democrat of Michigan, left, and Kerry Killinger, the ex-chief executive of Washington Mutual. The report singled out the bank for blame.

Published: April 13, 2011

A voluminous report on the financial crisis by the

United States Senate — citing internal documents and private communications of bank executives, regulators, credit ratings agencies and investors — describes business practices that were rife with conflicts during the mortgage mania and reckless activities that were ignored inside the banks and among their federal regulators.

The 650-page report, “Wall Street and the Financial Crisis: Anatomy of a Financial Collapse,” was released Wednesday by the Senate Permanent Subcommittee on Investigations, whose co-chairmen are

Carl Levin, a Michigan Democrat, and

Tom Coburn, a Republican of Oklahoma. The result of two years’ work, the report focuses on an array of institutions with central roles in the mortgage crisis:

Washington Mutual, an aggressive mortgage lender that collapsed in 2008; the Office of Thrift Supervision, a regulator; the credit ratings agencies

Standard & Poor’s and

Moody’s Investors Service; and the investment banks

Goldman Sachs and

Deutsche Bank.

“The report pulls back the curtain on shoddy, risky, deceptive practices on the part of a lot of major financial institutions,” Mr. Levin said in an interview. “The overwhelming evidence is that those institutions deceived their clients and deceived the public, and they were aided and abetted by deferential regulators and credit ratings agencies who had conflicts of interest.”

The bipartisan report includes 19 recommendations for changes to regulatory and industry practices. These include creating strong conflict-of-interest policies at the nation’s banks and requiring that banks hold higher reserves against risky mortgages. The report also asks federal regulators to examine its findings for violations of laws.

The report adds significant new evidence to previously disclosed material showing that a wide swath of the financial industry chose profits over propriety during the mortgage lending spree. It also casts a harsh light on what the report calls regulatory failures, which helped deepen the crisis.

Singled out for criticism is the Office of Thrift Supervision, which oversaw some of the nation’s most aggressive lenders, including Countrywide Financial, IndyMac and Washington Mutual, whose chief executive was Kerry Killinger. Noting that the agency’s officials viewed the institutions it regulated as “constituents,” the report said that the office relied on bank executives to correct identified problems and was reluctant to interfere with “even unsound lending and securitization practices” at Washington Mutual.

The report describes how two risk managers at the bank were marginalized by its executives. One of them told the committee that executives began providing the regulator with outdated loss estimates as the mortgage crisis widened. After the risk manager told regulators that the estimates it had received were dated, Mr. Killinger fired him.

From 2004 to 2008, for example, the regulatory office identified more than 500 serious deficiencies at Washington Mutual, yet did not force the bank to improve its lending operations, according to the report. And when the Federal Deposit Insurance Corporation, the bank’s backup regulator, moved to downgrade the bank’s safety and soundness rating in September 2008, John M. Reich, the director of the Office of Thrift Supervision, wrote an angry e-mail to a colleague. Referring to Sheila Bair, the F.D.I.C. chairwoman, he wrote: “I cannot believe the continuing audacity of this woman.” Washington Mutual failed two weeks later.

The office was abolished last year, and its operations were folded into the Office of the Comptroller of the Currency. Mr. Reich declined to comment. A lawyer for Mr. Killinger did not respond to a request for comment.

The report was produced by the same Senate committee that conducted an 11-hour hearing last April with Goldman executives and employees of its mortgage unit, who testified about their trading and securities underwriting practices.

At the hearing, some lawmakers questioned Goldman’s assertion that it had not bet against the mortgage market as real estate prices collapsed. And on Wednesday, Senator Levin pointed out that his committee had found 3,400 places in Goldman documents where its officials used the phrase “net short,” a reference to negative bets.

“Why would Goldman deny what was so obvious, that they were engaged in a huge short in the year 2007?” Senator Levin asked in a press briefing Wednesday morning. “Because they gained at the expense of their clients and they used abusive practices to do it.”

The report uncovered a new aspect of Goldman’s mortgage activity during 2007. That year, as Goldman tried to build its bet against housing, the report says, it drove down the cost of shorting the mortgage market by squeezing those who had made negative bets. Goldman tried to put on the squeeze, the report noted, so that it could add to its negative bets more cheaply and protect itself against the housing collapse.

Because Goldman was a large dealer in the marketplace, it had the power to drive prices in a certain direction. The report quotes from the self-evaluation of Deeb Salem, a mortgage trader, who wrote: “We began to encourage this squeeze, with plans of getting very short again.” He added, “This strategy seemed do-able and brilliant.”

Michael Swenson, head of trading in the structured product group at Goldman and Mr. Salem’s superior, also referred to the short squeeze, according to Senate investigators. In an e-mail, Mr. Swenson said that Goldman should “start killing” investors who were betting against mortgages. In testimony before the committee, however, he said he was simply trying to add balance to the market.

Goldman abandoned its plan in June 2007 when two Bear Stearns hedge funds collapsed because of bad mortgage bets.

A Goldman spokesman said in a statement: “While we disagree with many of the conclusions of the report, we take seriously the issues explored by the subcommittee. We recently issued the results of a comprehensive examination of our business standards and practices and committed to making significant changes that will strengthen relationships with clients, improve transparency and disclosure and enhance standards for the review, approval and suitability of complex instruments.”

The report also sheds new light on the bundling and trading of mortgages at Deutsche Bank, which had also made negative bets in that market.

Unlike Goldman, Deutsche Bank has not been accused of wrongdoing by government investigators. But the Senate report focuses on a trader named Greg Lippmann, who has since left the bank to join a hedge fund.

Mr. Lippmann was vocally negative about housing as early as 2005 and brought his idea of shorting the market to professional investors on Wall Street. He described risky mortgage securities before the crisis as “pigs,” according to the report. When he was asked to buy one such mortgage security, he responded that he “would take it and try to dupe someone,” according to the report.

Mr. Lippmann persuaded Deutsche to let him build a large short position, reaching $5 billion by 2007, the report says. The bank still lost money on other positive mortgage bets, but Mr. Lippmann’s trade helped reduce the company’s overall loss.

The report focused on one Deutsche collateralized debt obligation from 2006, called Gemstone VII, and described how Deutsche and other banks made $5 million to $10 million for every deal like Gemstone they created. In 2006 and 2007, banks created about a trillion dollars of C.D.O. deals — the most complex type of mortgage security and the instruments that sent the lending craze to dizzying heights.

In e-mails provided to the committee, Mr. Lippmann called the bank’s operation a “C.D.O. machine” and characterized such securities as a “Ponzi scheme.” But when the committee interviewed Mr. Lippmann, he backtracked, saying that his colorful descriptions were used to defend his negative view of the market.

In the Senate interview, Mr. Lippmann also said that he thought he was the person who persuaded the American International Group to stop writing insurance on mortgage securities. He told the committee that the head of the Deutsche Bank group that put together C.D.O.’s was upset when Mr. Lippmann persuaded A.I.G. to exit the business in 2006. Without A.I.G. there to insure the instruments, it would be harder to keep these lucrative factories humming.

Mr. Lippmann declined to comment on Wednesday.

Michele Allison, a spokeswoman for Deutsche Bank, said that the e-mails and other documents cited in the report indicated the divergent views within the bank about the housing market. “Despite the bearish views held by some, Deutsche Bank was long the housing market and endured significant losses,” she said in a statement.

reflections on regulation, law and public policy

April 15, 2011

By jennifer taub

William Blake’s The Marriage of Heaven and Hell came to mind, late Wednesday night as I waded through “Wall Street and the Financial Crisis: Anatomy of a Financial Collapse.” That is, the freshly-released bipartisan report from the Senate’s Permanent Subcommitee on Investigations. The Levin-Coburn Report, named for Subcommittee Chairman, Carl Levin (D-MI) and Ranking Minority Member, Tom Coburn (R-OK) came to the reasonable conclusion that:

“[T]he [2008] crisis was not a natural disaster, but the result of high risk, complex financial products; undisclosed conflicts of interest; and the failure of regulators, the credit rating agencies, and the market itself to rein in the excesses of Wall Street.”

This is not a remarkable finding, even endorsed by both political parties. Some controversy has emerged, however, from comments made by Senator Levin when the report was released. Levin said that referrals to the Justice Department and Securities and Exchange Commission would be made. In particular, the Senator reportedly suggested that Goldman Sachs CEO, Lloyd Blankfein, who testified before the subcommittee last April, should be criminally investigated by federal prosecutors for perjury. However, according to the Financial Times, Coburn is not happy and “The two men must now hammer out whether, in fact, those referrals are made.”

But, why Blake? Here’s the connection. I have already reviewed an array of books, studies, reports, articles, editorials, charts, conference papers, films, blog posts, testimony, draft bills, final legislation, legal memoranda, notices for proposed rulemakings, comment letters and final implementing rules addressing this topic. Additionally, I am working on my own book concerning the legal and regulatory causes and responses to the Financial Crisis. So, before facing another 639 pages, (including more than – gasp – 2,800 footnotes), I paused for a moment to ask myself — haven’t I read enough? In response, perhaps as a sort of pep talk, I remembered Blake’s:

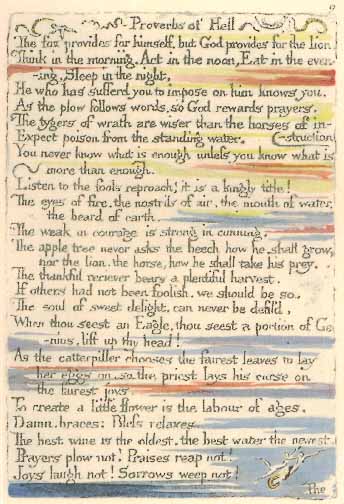

“You never know what is enough unless you know what is more than enough.”

Okay, then. Even if to some, another Financial Crisis report resembles a bland bowl of gruel, like Dickens’s young Oliver Twist, I say, “Please sir, I want some more.”

Fortunately, the Levin-Coburn Report is a bit tastier than that. It serves up four case histories of the blameworthy including: (1) high-risk mortgage lenders (Washington Mutual), (2) failed regulators (the Office of Thrift Supervision), (3) credit rating inflators (Moody’s and S&P), and (4) abusive investment banks (Goldman Sachs and Deutsche Bank.) The Report devotes more than 200 pages to Goldman alone, with a dozen alleged conflicts of interest on pages 602-603. Reflecting this emphasis, perhaps, a good portion of the early news coverage focuses on this bank.

Also, for those who followed the Subcommittee hearings in April 2010, including a from-breakfast-till-after-dinner grilling of the Taibbi-branded “vampire squid” investment bankers, the heavy Goldman flavor should be no surprise. That hearing (which can be watched here), began with a team of Goldman traders, including the “Fabulous Fab” Tourre and ended with Blankfein. Memorable moments included Senator Levin quoting Goldman employee emails that had described various structured securities as “shitty” and “crap pools.” At the time, it made me wonder whether those who sell investments called “crap pools” might want to reconsider referring to their business practices as “God’s work.”

Other highlights of that hearing included comments by CFO, David Viniar, now notably excerpted in the Academy Award-Winning documentary film, The Inside Job. When asked by Senator Levin how he felt about employees sending emails to each other calling an investment a “shitty deal,” Viniar responded, “I think that’s very unfortunate to have on email.” After additional questions, Viniar replied that he also thought it was “a very unfortunate thing for anyone to have said in any form” and finally that selling such a product was “unfortunate as well.”

The emphasis at the hearing and in the Levin-Coburn Report were conflicts of interest. Correspondingly, the Levin-Coburn Report highlights various purported conflicts at Goldman. One example was the Hudson 1 transaction. For this synthetic CDO, Goldman wore many hats, “including selecting assets and serving as the underwriter, initial purchaser of the CDO securities, collateral put provider, senior swap counterparty, and credit protection buyer.” Goldman represented that its interests were aligned with investors, pointing to the $6 million equity investment it made in Hudson. However, what Goldman allegedly did not reveal was that it also maintained a proprietary $2 billion short position. In addition, Goldman may have implied that Hudson assets (the credit default swaps) had come from outside sources when they were all produced and priced at Goldman. Ultimately, the Report states the firm collected $1.7 billion in gross revenues from the transaction and recorded a $1.35 billion profit. In contrast, the 25 Hudson investors lost all their money, as the Report notes “Today, Hudson securities are worthless.” Indeed, just three months after issuing the Hudson securities, a Goldman trader wrote that an investor’s “likelihood of getting principal back is almost zero.”

In addition, the Levin-Coburn report provides 19 recommendations for reform, summarized on pages 12 – 14. These recommendations are largely directed at federal regulators, suggesting essentially that they act to make lending less risky, regulators more bold, credit ratings reflect reality and investment banks less abusive. None of these recommendations appear to require new legislation. Instead, the Report would have the regulators use either long-existing or newly-granted authority under the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”).

Back to Blake. “You never know what is enough unless you know what is more than enough.” What would “more than enough” of the Financial Crisis coverage look like?

Well, we have not had “more than enough” accountability. Comparatively, after the Savings and Loan Crisis of late 1980s, more than 1,000 bank officials were prosecuted and around 800 went to jail. So far, as Gretchen Morgenson and Louise Story reported in yesterday’s New York Times, “no high-profile participants in the disaster have been prosecuted.” Alas, some of the easy targets for criminal cases have been customers, as Joe Nocera revealed earlier this month in his column, “In Prison for Taking a Liar Loan.”

We have not had “more than enough” safeguards restored to prevent a future catastrophe. Indeed, even the embarrassingly lax culture of the OTS, seemingly abolished by Dodd-Frank, as discussed on page 241, may live on inside the Office of the Comptroller of the Currency (“OCC”). Thus, it is particularly helpful that the Report reminds us of the OTS track record, “a proximate cause of the financial crisis.” For example, OTS identified over 500 serious deficiencies at Washington Mutual over a five year period from 2004 to 2008. However, the regulator did not lower the bank’s safety and soundness rating and it did not begin enforcement until 2008 when the $300 billion bank was on the brink of collapse. Eventually, the secondary regulator, the FDIC, through its Chairman Sheila Bair, stood up to Wamu by simply contacting the bank to alert them of a likely safety and soundness downgrade. When she did so, John Reich, the OTS director shot off an email to a colleague, complaining, “I cannot believe the continuing audacity of this woman.”

Certainly, we have not had “more than enough” audacious regulators like Bair. Along these lines, we are still waiting hopefully for the appointment of Elizabeth Warren to head the Consumer Financial Protection Bureau, as discussed here. We have not had “more than enough” redress for those fraudulently induced to enter into risky and expensive mortgages. There has not been “more than enough” ability for homeowners who are underwater on their mortgages to shrink their loan principal balances, while this mode of deleveraging when asset values decline is commonplace for other assets in bankruptcy proceedings. We have not had “more than enough” debunking myths about the Financial Crisis, as described in part 1 here and part 2 here.

Returning to Blake. There is a second reason that he came to mind in relation to the work of the Levin Subcommittee. That would be the title. The Marriage of Heaven and Hell. Marriage. The subcommittee launched its first of four hearings on April 13, 2010, one year ago to the day the Levin-Coburn Report was released. An anniversary gift. How thoughtful. Paper is the traditional first anniversary gift. It’s okay that the Levin-Coburn Report is digitized. So, what should we hope for next year? Well, a traditional second wedding anniversary gift is cotton. Here’s a hint. For next year’s gift to the American people, I’m thinking some nice one piece cotton jumpsuits in orange. Or maybe a poly/cotton blend, I’m not choosy. But, make sure they have white collars.

WASHINGTON – A few days ago, I joined with Sen. Tom Coburn of Oklahoma to release a bipartisan report on the causes of the financial crisis that pushed us into the recession that continues to afflict families in Michigan and across the country.

The report is the product of more than two years of work by the Senate Permanent Subcommittee on Investigations, which I chair. Last year, our subcommittee held four hearings on what we uncovered, and the 600-page report expands on what we learned from those hearings, hundreds of witness interviews and millions of pages of documents.

The financial crisis was a man-made economic assault, the product of reckless risk-taking and rampant conflict of interest on the part of some big banks, mortgage companies and credit rating agencies. The recession that followed the crisis devastated Michigan’s economy; it cost more than 400,000 Michigan jobs; it cost thousands of Michiganians their homes; and it nearly decimated our domestic auto industry. That’s why it’s so important for Michigan and the country that we get a clear picture of the causes of the crisis, to try to make sure it never happens again.

What did we learn in our investigation? Conflict of interest is the common thread that runs through this whole sordid story. Our bipartisan report pulls back the curtain on shoddy, risky and deceptive practices. We showed that major financial institutions deceived their clients and the public, aided and abetted by conflicted and deferential regulators and credit rating agencies.

Sen. Coburn, who with his staff made major contributions to our investigation, put it well: “The free market has helped make America great, but it only functions when people deal with each other honestly and transparently. At the heart of the financial crisis were unresolved, and often undisclosed, conflicts of interest.”

Washington Mutual Bank, the nation’s largest thrift, issued thousands of mortgages in Michigan that later failed and resulted in foreclosures that devastated neighborhoods. Executives at WaMu, as the bank was known, pursued a high-risk strategy of selling dubious and often fraudulent mortgages and pushing customers into high-risk, high-interest loans so WaMu could reap higher profits, then turning these mortgages into toxic assets that the bank used to pollute the financial system.

We showed how WaMu’s main federal regulator, the Office of Thrift Supervision, knew all along about major problems with the bank’s mortgages. But instead of cracking down, OTS treated WaMu with kid gloves, refusing to act on repeated warnings by its examiners and blocking efforts by other regulatory agencies to act. One problem was that fees from WaMu made up a big chunk of the agency’s annual budget. In 2008, WaMu collapsed under the weight of its junk loans and is now the largest bank failure in U.S. history.

We also examined how credit rating agencies that were supposed to provide objective opinions about the quality of mortgage-related securities gave high ratings to toxic assets. The credit rating agencies knew they would lose lucrative business from investment banks if they gave lower ratings.

And we showed how investment banks such as Goldman Sachs assembled toxic securities, misled the clients they sold them to, and then profited by betting against the very same investments they had sold to their clients.

Our report, the product of two years of hard work by my subcommittee, goes into great detail in each of these areas, and I’d encourage you to go to my website, levin.senate.gov, to read the entire report.

Last year, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act, which addresses many of the problems our investigation identified. For example, it eliminated OTS, the regulatory office that failed so completely to rein in WaMu’s reckless lending. And it included a provision that Sen. Jeff Merkley of Oregon and I fought for, limiting the ability of banks to make risky investments for their own profit, and prohibiting them from betting against the same investments that they sold to clients.

Our report includes 19 new recommendations to further curb Wall Street excesses and conflicts of interest. Those recommendations, like the Dodd-Frank Act itself, will be opposed by some members of the financial industry who want to continue their risk-taking ways. I’ll do all I can to make sure that federal regulators act with forcefulness and determination to fully implement the Dodd-Frank reforms.

Michigan and the nation can’t afford another crisis from Wall Street. Understanding how the last crisis happened is vital to preventing the next one, and our report is designed to contribute to that effort.

{kind=link}

The dollar can be tendered for circulation legally only within the jurisdiction of the continental United States. Any attempt to impose the currency on the outside world though threat, or manipulation or both is reflective of an uncivil culture and society.

ReplyDeleteAnd any attempt to coerce the same through military might is outright criminal. History has never been kind to people who are criminals however white they may be.

ümraniye alarko carrier klima servisi

ReplyDeleteataşehir samsung klima servisi

çekmeköy mitsubishi klima servisi

ataşehir mitsubishi klima servisi

maltepe vestel klima servisi

kadıköy vestel klima servisi

maltepe bosch klima servisi

kadıköy arçelik klima servisi

kartal samsung klima servisi

Good content. You write beautiful things.

ReplyDeletevbet

korsan taksi

taksi

hacklink

mrbahis

vbet

sportsbet

hacklink

mrbahis

Good text Write good content success. Thank you

ReplyDeletepoker siteleri

slot siteleri

tipobet

betmatik

betpark

kibris bahis siteleri

mobil ödeme bahis

kralbet

This post is on your page i will follow your new content.

ReplyDeletesportsbet

sportsbet giriş

mrbahis

betgaranti.online

mrbahis.co

sportsbet

casino siteleri

sportsbetgiris.net

mrbahis giriş

https://saglamproxy.com

ReplyDeletemetin2 proxy

proxy satın al

knight online proxy

mobil proxy satın al

81M