“The Bear Market Economics Phenomenon” is an observation of Political Economics. Wall Street Admits: ‘We Got Rich Off the Backs of Workers’ thus creating the Bear Market. The Bear Market is America's default war.

The ethic of Wall Street is the ethic of celebrity. It is fused into one bizarre, perverted belief system and it has banished the possibility of the country returning to a reality-based world or avoiding internal collapse. A society that cannot distinguish reality from illusion dies.

This site may contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in an effort to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. we believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law.

In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. For more information go to: http://www.law.cornell.edu/uscode/17/107.shtml

If you wish to use copyrighted material from this site for purposes of your own that go beyond ‘fair use’, you must obtain permission from the copyright owner.

FAIR USE NOTICE FAIR USE NOTICE: This page may contain copyrighted material the use of which has not been specifically authorized by the copyright owner. This website distributes this material without profit to those who have expressed a prior interest in receiving the included information for scientific, research and educational purposes. We believe this constitutes a fair use of any such copyrighted material as provided for in 17 U.S.C § 107.

FAIR USE NOTICE FAIR USE NOTICE: This page may contain copyrighted material the use of which has not been specifically authorized by the copyright owner. This website distributes this material without profit to those who have expressed a prior interest in receiving the included information for scientific, research and educational purposes. We believe this constitutes a fair use of any such copyrighted material as provided for in 17 U.S.C § 107.

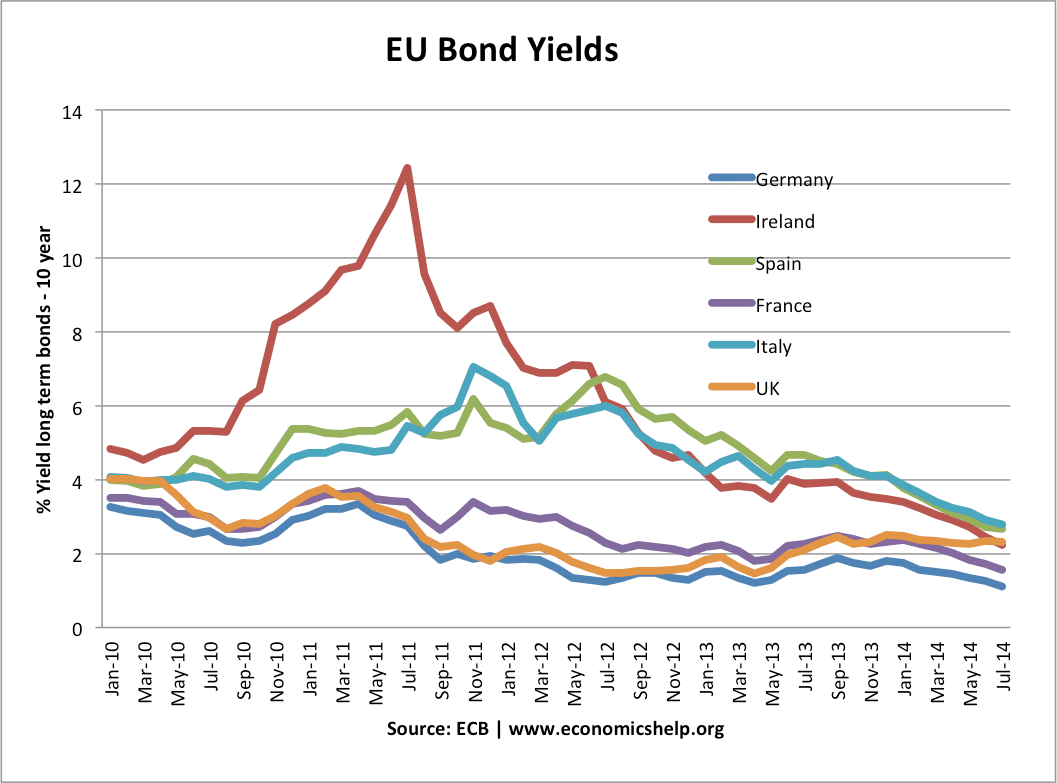

In 2007, EU economies, on the surface, seemed to be doing relatively well – with positive economic growth and low inflation. Public debt was often high, but (apart from Greece) it appeared to be manageable assuming a positive trend in economic growth.

Bank Loses. During the credit crunch, many commercial European banks lost money on their exposure to bad debts in US (e.g. subprime mortgage debt bundles)

Recession. The credit crunch caused a fall in bank lending and investment; this caused a serious recession (economic downturn). See: cause of recession

Fall in House Prices. The recession and credit crunch also led to a fall in European house prices which increased the losses of many European banks.

Recession caused a rapid rise in government debt. The recession caused a steep deterioration in government finances. When there is negative growth, the government receive less tax: (less people working = less income tax; less people spending = less VAT; less company profits = less corporation tax e.t.c. ) (The government also have to spend more on unemployment benefits.)

Rise in Debt to GDP ratios. The most useful guide to levels of manageable debt is the debt to GDP ratio. Therefore, a fall in GDP and rise in debt means this will rise rapidly. For example, between, 2007 and 2011, UK public sector debt almost doubled from 36% of GDP to 61% of GDP (UK Debt – and that excludes financial sector bailout). Between 2007 and 2010, Irish government debt rose from 27% of GDP to over 90% of GDP (Irish debt) .

Markets had assumed Eurozone debt was safe. Investors assumed that with the backing of all Eurozone members there was an implicit guarantee that all Eurozone debt would be safe and had no risk of default. Therefore, investors were willing to hold debt at low interest rates even though some countries had quite high debt levels (e.g. Greece, Italy). In a way, this perhaps discouraged countries like Greece from tackling their debt levels, (they were lulled into false sense of security).

Increased Scepticism. However, after the credit crunch, investors became more sceptical and started to question European finances. Looking at Greece, they felt the size of public sector debt was too high given the state of the economy. People started to sell Greek bonds which pushes up interest rates) see: relationship between bonds and yields)

No Strategy. Unfortunately, the EU had no effective strategy to deal with this sudden panic over debt levels. It became clear, the German taxpayer wasn’t so keen on underwriting Greek bonds. There was no fiscal union. The EU bailout never tackled fundamental problems. Therefore, markets realised that actually Euro debt wasn’t guaranteed. There was a real risk of debt default. This started selling more – leading to higher bond yields.

No Lender of Last Resort. Usually, when investors sell bonds and it becomes difficult to ‘roll over debt’ – the Central bank of that country intervenes to buy government bonds. This can reassure markets, prevent liquidity shortages, keep bond rates low and avoid panic. But, the ECB made it very clear to markets it will not do this. (see: failures of ECB) Countries in the eurozone have no lender of last resort. Markets really dislike this as it increases chance of a liquidity crisis becoming an actual default.

For example, UK debt has risen faster than many Eurozone economies, yet there has been no rise in UK bonds yields. One reasons investors are currently willing to hold UK bonds is that they know the Bank of England will intervene and buy bonds if necessary.

Uncompetitiveness

Eurozone countries with debt problems are also generally uncompetitive with a higher inflation rate and higher labour costs. This means there is less demand for their exports, higher current account deficit and lower economic growth. (The UK became uncompetitive, but being outside the Euro, the Pound could depreciate 20% restoring competitiveness. See more at Two speed Europe

Poor Prospects for Growth

People have been selling Greek and Italian bonds for two reasons. Firstly because of high structural debt, but also because of very poor prospects for growth. Countries facing debt crisis have to cut spending and implement austerity budgets. This causes lower growth, higher unemployment and lower tax revenues. However, they have nothing to stimulate economic growth.

They can’t devalue to boost competitiveness (they are in the Euro)

They can’t pursue expansionary monetary policy (ECB won’t pursue quantitative easing, and actually increased interest rates in 2011 because of inflation in Germany)

They are only left with internal devaluation (trying to restore competitiveness through lower wages, increased competitiveness and supply side reforms. But, this can take years of high unemployment.

Individual Cases

Ireland’s debt crisis was mainly because the Irish Government had to bailout their own banks. The bank losses were massive and the Irish government needed a bailout to pay for their own bail-out

Greece. Greece had a very large debt problem even before joining Euro and before the credit crisis. The credit crisis exacerbated an already significant problem. The Greek economy was also fundamentally uncompetitive.

Italy’s debt crisis – long term structural problems. Very weak growth prospects. Political instability

Summary of Main Causes of Debt Crisis

High structural debt before crisis. Exacerbated by ageing population in many European countries.

Recession causing sharp rising in budget deficit.

Credit crunch causes losses for Commercial banks. Investors much more cautious and fearful of default in all types of debt.

Southern European economies uncompetitive (higher labour costs) but can’t devalue to restore competitiveness. This causes lower growth and lower tax revenues in these countries.

No Lender of last resort (like in UK and US) makes markets nervous of holding Eurozone debt.

No effective bailout for a country like Italy.

Fears of default raise bond yields, but this makes it much more expensive to pay interest on debt. e.g. cost of servicing Italian debt has risen meaning they will have to raise €650bn ($880bn) over next three years. It become a vicious spiral. Higher debt leads to higher interest rate costs making it more difficult to repay.

One issue has been helped. Action by the ECB has led to a fall in bond yields. This willingness to intervene in the bond market has calmed investors and led to lower bond yields. However, the economy remains stagnant with low growth.

The European sovereign debt crisis! It -- wait, come back. This is interesting, we promise. The debt crisis is one of the biggest stories of the year, maybe of the decade. If you're American, how can you tell whether the situation across the pond affects you?

Take our quiz to find out:

1) Do you like money?

2) Would you rather have money than not have any money?

If you answered "yes" to either of the above, then the Europe situation probably has bearing on your life. Here's a quick explanation of what's happened.

(More of a picture person? Scroll down for graphics that help to explain the crisis)

WHAT IS THE EUROPEAN DEBT CRISIS?

In its most basic form, it's just this: Some countries in Europe have way too much debt, and now they risk not being able to pay it all back. Simple!

There's more to it than that, of course, but when people talk about the "crisis," what they're worried about is that a big, scary, flashpoint event will happen -- like one or more of the eurozone countries defaulting on its debts -- causing investors to panic and triggering a massive banking shock.

The possibility also looms that one or more countries will pull out of the eurozone -- the 17-nation bloc that use the euro currency, which has been around since 1999. Should any of the eurozone nations drop out of this group, it could lead to a rash of bank failures in Europe, and possibly in the United States as well. Under these circumstances, people and businesses who need money might not be able to get any. We'd be looking at depression for Europe and recession for the rest of the world. Some people argue that an orderly, controlled eurozone break-up would be a good thing for certain struggling debtor nations. Still, even this relatively benign scenario carries economic fallout for Europe and maybe beyond.

HOW DID THIS HAPPEN?

The reason everyone is freaking out now is that while some eurozone countries are relatively sound from an economic standpoint, other countries are way over-leveraged, meaning they have too much debt relative to the size of their economies. And the troubles of a few countries could end up affecting everyone, yoked together under one currency for the last decade -- even though their economies functioned according to different habits and enjoyed very different degrees of financial health.

Portugal, Ireland, Italy, Greece and Spain -- gathered under the unfortunate acronym PIIGS -- are some of the most highly leveraged eurozone countries, and most people think that if a disaster happens, it will start with one of them. Italy's debt is 121 percent the size of its economy. For Ireland, that figure is 109 percent. In Greece, it's 165 percent.

The PIIGS took different paths to this scenario. Ireland, for example, underwent a massive real estate bubble, and its banks sustained giant losses. The Irish government wound up rescuing its banks, and now the country is burdened under a huge debt load.

Spain, which now has a 22 percent unemployment rate, also experienced a huge housing bubble. The country didn't indulge in excessive borrowing -- rather, it ended up with high deficits because it couldn't collect enough tax revenue to cover its expenses.

Greece, on the other hand, not only borrowed beyond its means, but exacerbated the problem with lots of overspending, little economic production to make up the difference, and some creative bookkeeping to prevent eurozone authorities from realizing the true extent of the situation.

The deficits weren't piling up everywhere. Countries with strong economies like Germany and France were keeping their output high and their debt at a manageable level. But when 17 nations use the same currency, trouble spreads quickly.

Now that the size of the PIIGS' debt has become clear, investors are getting more and more reluctant to buy bonds from European countries, since many of those countries are heavily in debt -- and the ones that aren't in debt look like they might have to assume responsibility for the ones that are. Investors don't want to put their money into bonds if they think they might not eventually get that money back. And governments in Europe have a lot of debt and not much money -- and it's not clear how they're going to correct this.

WHOSE FAULT IS IT?

Blame often gets cast on the "irresponsible" countries who borrowed too much, taking advantage of the low interest rates available to all euro member nations. However, many argue that it's not right in all cases to blame indebted governments for their own situation, since not every country with high deficits actually engaged in reckless borrowing.

Others say the euro currency itself is to blame -- arguing that the idea that a single currency could meet the needs of 17 different economies was inherently flawed. Typically, a country's central bank can adjust a nation's money supply to encourage or inhibit growth as a way of dealing with economic turmoil. However, the nations yoked together under the euro frequently haven't had that option.

If Spain and Germany hadn't both spent the last several years on the euro, for example, then they wouldn't have been able to borrow at the same low interest rates -- an interest rate set by the European Central Bank, and one that made more sense for Berlin than for Madrid.

Greece might still be shouldering huge debts if not for the euro, but maybe it wouldn't be in a position to take down the rest of Europe with it. And if the PIIGS all still had their own individual currencies, they might be able to export their way out of the mess they're in -- selling goods on the international market until their respective situations were a little less dire. But as it is, they can't.

Alternatively, if you like, you could say the interconnectedness of the modern financial industry is to blame. That's certainly a reason default by Italy or a departure of the eurozone by a fed-up Germany -- to name two examples -- could reverberate around the world.

FROM THE OLD WORLD TO THE NEW

The crisis in Europe could end up affecting the U.S. in some very direct ways. American banks have billions of dollars at risk in European banks. And while that's actually a relatively small fraction of U.S. banks' holdings, the indirect damage could be greater: U.S. business owners could be facing a credit crunch if overseas banks topple.

Further, the U.S. stands to suffer huge trade losses if Europe slips into a recession. Fourteen percent of all U.S. exports go to the eurozone, so weak consumption in Europe spells trouble in the States.

At the moment, a downturn in Europe is the last thing the U.S. needs. Growth is slow in America, and millions of people aren't working who'd like to be. The U.S. needs to be producing and exporting more, not less, and it's already hard enough for small businesses in the States to get credit from banks.

The Great Recession technically ended in 2009, but for a lot of people -- people in poverty,people who can't afford food, people working long hours for low wages -- it feels like things are as bad as ever. A financial emergency in Europe, triggered by some event that sends investors running for cover, could take all of America's problems and make them bigger.

WHAT HAPPENS NEXT?

This is a fast-moving story, and by the time you read this, circumstances may have already changed. As of this writing, though, all of Europe is basically trying to do damage control. European Union authorities have put together a funding package of 150 billion euro for the International Monetary Fund to disperse to debt-stricken eurozone nations, and many countries are using inventive asset-juggling tricks to get capital into their banks without officially bailing anyone out.

Earlier this month, eurozone authorities drew up a tentative proposal to enforce stricter consequences on countries that borrow beyond an agreed-upon limit. The deal would also require eurozone nations to balance their budgets, and aims to bring members of the currency bloc into greater sync from a fiscal standpoint.

EU leaders will meet again on January 30 to further discuss this deal. In the meantime, European governments are doing all they can to soothe investors -- a task made harder by ominous rumblings from credit rating agencies like Moody's, Fitch and Standard & Poor's, which have all downgraded or threatened to downgrade numerous countries and financial institutions in the eurozone and elsewhere. (You may remember Standard & Poor's from the fun downgrade debacle of this past summer, when that agency lowered the United States' sovereign credit rating one notch and caused markets to spaz out.)

At the moment, it's not clear whether any of the curative measures in the works will allow Europe to avoid a major financial downturn. Some onlookers are skeptical that the eurozone nations can reach a workable deal, since the countries have a poor track record of working together on financial matters. And things are likely to remain on a hair trigger even if a deal progresses, since bank-to-bank relationships rely on trust and credibility, and even the perception of a crisis could quickly become self-fulfilling.

Meanwhile, as all this is going on, troubled eurozone countries are pledging to cut back government spending to show they can be trusted -- even though this results in financial misery for the people in those countries, and will in all likelihood make it harder for Europe's economy to gain any momentum in the months to come.

Is there anything you can do about the situation in Europe? Not really -- except keep an eye on it. Disaster isn't a foregone conclusion at this point, but if things do go south on the Continent, the business climate in America will likely get worse before it gets better. You'll want to be able to see that coming if it does.

Below are graphics featuring a country-by-country break down of some of the most important indicators of the crisis :

The fever that gripped the U.S. following the attacks of September, 11, 2001 demonstrated that manufacturing a shared enemy did little to create a deeper commonality of interests amongst nominal citizens. Whatever one may think about the specifics of the attacks— the motives of the attackers, their choice of targets or the veracity of official explanations, it would have required a full scale assault by an established military to destroy as many lives and communities as American born and bred bankers did through predatory mortgage lending in the housing boom and bust. And as much as official apologists would like to deny it, this destruction is wholly in keeping with the market outcomes that now constitute the base credo of the market-state.

The paper-thin bravado that sent heavily armored children and young adults to slaughter innocents in Afghanistan and Iraq for the benefit of Bechtel, Northrup Grumman and Exxon Mobil found its domestic truth in the quivering puddles that had supported the wars suddenly wondering how they were going to feed themselves and their children with their jobs outsourced and their homes in foreclosure. A fortunate few saw their fealty to the system of economic and social dispossession rewarded through the spectacle of social dissolution, through their neighbor’s bounty of cheaply-made goods strewn across suburban and ex-urban lawns as sheriffs and their agents made room for fresher members of the tenuous classes.

Graph (1) above: eight years after the onset of the Great Recession the storyline of recovery is fraying around the edges. Real Median Household Income, the statistic conceived to obfuscate more straightforward wage data through aggregation, continues its downward trajectory. When associated with unforgiven and re-imposed household debt a picture of Great Depression-style debt deflation emerges for the toiling and dispossessed classes. The great public mystery of renewed urban violence is why its conspicuous relation to economic re-immiseration remains so well hidden? Overlaid maps of predatory banking in the early-mid 2000s with social dissolution and urban decay today correlate 1:1. An invading army could hardly have achieved this level of destruction without advanced weaponry and a deep hatred for the peoples being invaded. Data source: Census Bureau. Image source: flickr.com.

After eight years of alleged economic ‘recovery’ the pre-existing lines of social division are once again being clarified as class, race and geography separate the recovered from those left behind. Recent data from the Census Bureau (Graphs (1, 3)) illustrates the ongoing downward trajectory of real (inflation-adjusted) household incomes for all but the richest. This is more than simple ‘income inequality,’ it is evidence that very particular class interests are being served by the political establishment. The incomes and wealth of the richest have been recovered through official policies with little regard for the other 99.97% of the population. Leftish economists repeatedly claim that political dysfunction explains policy paralysis while policies that benefit the rich have met no resistance.

Graph (2) above: food stamp (SNAP- Supplemental Nutrition Assistance Program) usage and stock prices (Wilshire 5000) have risen together over the last twenty five years putting a lie to ‘trickle-down’ theories of the social benefit of rising financial asset values. Technical quibbles aside (neither series is scaled to relevant bases), of relevance is the catastrophic rise in the need for food assistance since 2007 as stock prices have been supported by government and quasi-government (Federal Reserve) policies. Rising stock prices benefit the rich alone because the rich own most of the stock. Data source: St. Louis Federal Reserve. Image source: alaskapublicemployees.com.

The Great Irrelevance

The great irrelevance of the moment, recently answered in the negative, of whether the Federal Reserve will raise interest rates ignores the obvious: it would if it could, but it can’t. The attendant spectacle of dedicated servants of Wall Street in contrived conniptions over ‘the plight of the poor’ would be laughable were it not for the ongoing social dissolution so in evidence. The trajectory of falling interest rates since 1982 ties directly to the increasing hold that financial operators have over capitalist economies. The falling price of credit (interest rates) led to its deep instantiation into every aspect of contemporary economic relations. The political victory for the existing order finds various and sundry advocates for the poor and toiling classes arguing that bank-friendly policies benefit the rest of us with little evidence on their side.

Assertion of a unitary public interest ignores both that more direct (fiscal) policies would have more direct effect and that it is the very beneficiaries of banker-friendly policies (bankers) who are using their political power to preclude policies directly beneficial to the poor. It is hardly incidental that leading members of the Black ‘mis-leadership class’ (as the folks at Black Agenda Report have so named them) have been enlisted to use what little remains of their credibility to carry water for Wall Street in this regard. In recent history when interest rates were lowered to benefit bankers (the Greenspan ‘put’) the entirety of Black wealth disappeared into bank coffers. And that is the least of it— the social dissolution now seen across the country ties directly to decades of exploitative practices by capitalists using finance as a tool for economic exploitation.

National Democrats have been pushing the storyline of economic recovery even as major American cities are being torn apart by engineered economic devastation. Households have seen the largest and most sustained decline in incomes since the Great Depression as millions of prime-age workers sit idle, excluded from meaningful employment. National and international banks, Wall Street, sit on untenable levels of bad ‘assets’ that would (mechanically) decline in value if interest rates were ever raised. The social cruelty of the recovery meme lies in the destitution of those excluded from it along the axes of class and race. Leading, and generally thoughtful, economists proclaim that a second Great Depression was averted when whether one was or not depends very much on where one is sitting.

Just how cynical official efforts have been to push economic Pollyanna front-and-center is made evident through the economic ‘recovery’ storyline itself. ‘Household income’ replaced more direct measures of labor wages as women joined the workforce en masse in the 1970s. Where one wage-earner could support a family before the 1970s it required two to earn just a bit more a decade later. While generally put forward with a shrug by mainstream economists, real wages for most people haven’t fallen to the degree of recent years since the Great Depression. There are known methods of economic resolution— government jobs programs and targeted government spending, which would boost employment and wages. But these have been foregone in favor of monetary policies that boost housing values and financial asset prices.

Immaculate Bullshit

Eight years of selective economic reporting have succeeded in shifting the grounds of discourse from wholesale replacement of the established order to tinkering around the edges. And it isn’t that the already rich and those connected to (government supported) technology and financial centers haven’t seen recovery— many are as prosperous as ever. Eight years of government support for all things financial have reflated traditional bubble areas— stock and financial asset prices and home values in London, Manhattan and Southern California. The questions of what happened to the millions of foreclosures that were supposed to keep pressure on house prices, of the millions of missing prime-age workers who couldn’t afford to retire and of the mysterious, ongoing drop in median incomes were overtaken by engineered optimism, not answered.

Employment: If all workers dropped out of the labor force the unemployment rate would be zero. The three million prime-aged workers who dropped out since 2008 got it down to 5.1%. These are people who were working when there were jobs and who aren’t working now. How good a description of the state of labor markets is the unemployment rate then? Additionally, McJobs— tenuous employment at low wages with few if any benefits; have increasingly replaced the jobs that created the American Middle Class. Never far below the surface is the moral chide of the ‘lazy’ unemployed— that with an unemployment rate of 5.1% anyone who wants a job can get one. Or as Mitt Romney put it, why don’t poor parents simply lend their children the money to start their own businesses?

Incomes: As Graphs (1, 3) illustrate, real median household incomes have been declining since the late 1990s for most households and the trend shows no sign of abating. The more precise story ties to unemployment— ‘disappearing’ prime-age workers explain the drop more than declining wages for workers with jobs. This brings ‘household income,’ conceived to cover for falling ‘breadwinner’ wages from the pre-1970s economy, full circle with single ‘breadwinners’ once again supporting households in greatly diminished circumstances. What falling household incomes demonstrate is that the economic circumstances of most people fell off of the proverbial cliff around 2008 and have yet to see any ‘recovery.’ This leaves an increasing swath of working families one paycheck away from destitution or already there.

Wealth: To wallow in the obvious, wealth has always been the purview of the wealthy. Whatever one thinks of the Federal Reserve policies of the last eight years, they have led to full recovery of financial asset prices and luxury real estate. The wealthiest ten percent of the population owns eighty percent of financial assets with heavy concentrations at the top of the top one percent. Additionally, the high-end real estate owned by the rich has largely recovered while that on the lower end of the spectrum remains severely ‘under water’ (worth less than the mortgages against them). The ‘centrist’ economic argument that recovery for the rich alone is better than no recovery requires a view of class relations that is clearly not reciprocal.

Housing: Optimists have long been proclaiming a housing market recovery without answering the question of what happened to the mountain of foreclosures that were the result of the housing bust. The answer is making itself known in the Northeastern U.S. as years of bank ‘forbearance’ are being resolved through a new wave of foreclosures. Economic misery long hidden from view is being brought into tragic relief. Large areas of New York, New Jersey and Pennsylvania are seeing levels of foreclosures that will devastate lives and communities for decades to come. The Obama administration could have used bank bailout funds to ‘buy-down’ mortgage principal and the housing bust would be a distant memory. It chose to support bankers against the victims of their predatory practices instead.

Graph (3) above: the term ‘income inequality’ has disappeared from the headlines since Thomas Piketty made a splash with his book on the topic last year. This newly released data from the Census Bureau illustrates its central components— rising incomes for the rich and falling incomes for everyone else over the last decade. The start of the trend dates to the inception of the modern epoch of finance capitalism in the early 1980s coincident with Ronald Reagan’s version of tax cuts for the wealthy. The truth of stagnant wages and household incomes for most people puts a lie to ‘trickle-down’ theories that are now several decades past their expiration date. Of relevance is that this, and the data in Graph (1) above, is new— this is reporting on current circumstance, not that of several years ago that has since been resolved. Original source: Bloomberg.com.

Of all the corporate media propaganda which warps reality in America, one echoed statement makes me wretch more than any other, and that’s “the jobs straw man” in defense of laissez faire capitalism, a commonly-used device to declare that greed is good despite the damning evidence.

The jobs straw man exists to convince the public that the things which most hurt them are really good things, providing jobs, so they should not complain. This fools the vast majority of citizens, echoed as it is daily throughout the mainstream media without any attempt at balance, and stifling any reasonable debate.

I will describe how it’s used with lines beginning “Propaganda,” and follow those lines with facts that don’t air on TV news in the Land of the Free.

Propaganda: We must keep producing fossil fuels because it provides jobs.

We could create more jobs producing solar panels and wind turbines if we did so without the multi-million dollar salaries that go to the executives of existing carbon-based industries, and didn’t put so much of the profits into rewarding wealthy investors, and cut off government subsidies to Big Oil, Big Coal and Big Gas. In fact, most of the jobs from fossil fuels we use are abroad, in places like Saudi Arabia.

We’d also reduce the impact on global warming, while cleaning up the air quality, thereby serving the public interest.

Propaganda: We must support free trade because it provides jobs.

We produced far better paying jobs before the primary rival of American capitalism, the USSR, dissolved and capitalists realized they no longer had to compete for the loyalty of workers, since workers only had one place to go. Corporate bosses (to paraphrase Jefferson) never so loyal to so much as the spot on which they stand, moved jobs from the USA to the third world in response with what is euphemistically called “free trade.”

Nobody in corporate media ever asks those who’ve lost their jobs because of it, what they think of “free trade.” A small part of the US workforce is employed in “free trade,” but most workers are hurt by it. We would also have a much cleaner environment if workers produced products closer to where they would be used.

Propaganda: We must keep the largest military force on earth because it provides jobs.

For the money which goes into the US national security system, we could easily provide far more jobs doing something to improve the nation, such as rebuilding its infrastructure, creating a national mass transit system, or implementing a national health care system as exists in the rest of the industrialized world, actually improving things, rather than using the government primarily to provide security for the wealthy investors of the world.

The military/industrial complex is filled with fraud, waste and abuse. Billions of dollars often go missing and nobody is ever held accountable. It is nonsense to claim that this is a good way to provide jobs.

Propaganda: We must support capitalism because it provides jobs.

Many nations with mixed economies, that is partly socialist, enjoy much better average working conditions than do Americans, even though the USA is the wealthiest nation on earth. Workers in other major industrialized nations enjoy better pay and benefits, with lower and less severe unemployment (The number of unemployed in the US is always at least twice the official numbers).

There are countless more examples of things that go against the public interest justified by the jobs straw man in the mainstream press.

Listening to this nonsense one would think jobs are a primary concern of the establishment press and the business interests they represent. Nothing could be further from the truth.

American businesses lay off employees by the millions at the drop of a hat. Any hint of economic downturn and the workforce is jettisoned. Profits for transnational investors who don’t give a damn about the nation, the planet, or anything beyond profit comes before all else. Second, the multi-million dollar salaries of corporate executives are protected over any cost in jobs.

Arms must often be twisted for businesses to create jobs, with incentives such as tax breaks. Ironically, corresponding tax increases are not demanded of these companies when they lay off employees. In short they ask to be rewarded for hiring, but not punished for firing, having it both ways.

Jobs straw man statements are made in the mainstream press as if they are true, and are not questioned. If one listens to the TV journalists, where most Americans get their news, they will hear this nonsense pop up daily.

It is one of the reasons so many of our fellow citizens will “correct” us, if we should propose something better. We can’t interfere with the system, they will say, because it provides jobs.

The only time authorities in the corporate controlled press or corporate controlled government appear to “care” about jobs is when profits are threatened by proposals to cut military spending, clean up the environment or have the government actually do something on behalf of its citizens.

The propaganda works because the masses cannot see the forest for the trees. The statements are repeated like machine gun fire at us nonstop, blurring the senses. Until citizens understand how the propaganda works, they will be controlled by it.

Ben Bernanke, 2011. (Shirley Li/Medill DC via Flickr)

The 2008 financial crisis challenged many orthodox assumptions in finance and economics, including the proper role and accountability of central banks. The U.S. Federal Reserve, commonly known as the Fed, is the world’s most powerful central bank.

One major source of Federal Reserve power is its role as “lender of last resort,” lending directly to commercial banks through its so-called discount lending window. Traditionally, only commercial banks had access to the Fed’s discount lending since non-bank financial institutions were not subject to the same reserve and capital requirements as those imposed on banks. The other major source of the Fed’s power is its ability to purchase short-term Treasury securities. These restrictions on Fed lending and asset purchases helped support the central bank’s political independence from Congress and the White House by ensuring that Fed policy was socially neutral and did not favor particular sections of financial markets or particular private constituencies. But as the Federal Reserve’s lending and asset purchase powers expanded in unprecedented ways in 2008, these traditional restrictions were swept aside, exposing the flaws of central bank independence.

The Fed is also able to create money—U.S. dollars, also known as Federal Reserve notes—which means there is virtually no limit to the amount of money it can lend and no limit to the volume of assets it can purchase without adding to public-sector borrowing or deficits. During the 2008–2009 financial crisis, the Fed extended more than $16 trillion in low interest loans to all kinds of financial institutions in distress, including borrowers who traditionally lacked access to its discount window such as hedge funds and foreign commercial banks and central banks. Also, beginning in 2008, the Fed launched several asset purchase programs, known as “quantitative easing” (or QE), to purchase more than $3.5 trillion in U.S. Treasury securities and mortgage-backed securities (MBS).

But this expansion of the money supply is deceiving. Instead of lending out the funds pumped in by the Fed, banks have added more than $2.6 trillion to their excess reserves, on which the Fed has also paid them interest. This is similar to what happened during the Great Depression. Much of the money the Fed pushed into the banking system has not trickled down to the real economy.

Ben Bernanke, the Federal Reserve chairman when the QE programs were first launched, claimed that asset purchases would have a “wealth effect”: by the Fed purchasing bonds in such large amounts, bond prices would rise, yields would fall, and investors would shift into riskier securities, driving up the price of corporate shares and stock markets. Everyone would feel richer, businesses would invest and consumers would spend more. This seems much like the theory of “trickle-down” fiscal policy: that tax cuts for those with high incomes would be invested, thereby leading to the hiring of additional workers and spreading the benefits to the rest of the economy. But like the Bush administration’s tax cuts, the Fed’s monetary trickle-down has not worked so well. The Fed’s lending and asset purchase programs have effectively propped up Wall Street interests—big banks and financial markets—but they have also neglected the needs of Main Street, including the small community banks, small and moderate sized and family-owned businesses, unemployed and underemployed workers, and state and local governments.

The Federal Reserve’s response to the 2008 crisis is quite different from its “bottom up” approach in the Great Depression in the 1930s when it extended credit directly to Main Street businesses. Section 13(3) of the Federal Reserve Act allowed the Fed to lend directly, not just to big banks, but also to “individuals, partnerships, and corporations” in “unusual and exigent circumstances.” Another provision, section 13(b) (since repealed in 1958) authorized the Fed to make credit available for “working capital to established industrial and commercial businesses” with permissible maturities of up to five years and “without any limitations as to the type of security” for collateral. In total, the Fed made about $280 million available to small- and moderate-sized businesses. That was about 0.43 percent of GDP at the time, or about $65 billion in today’s terms.

In contrast, in the aftermath of the 2008 financial crisis, the Federal Reserve has consistently rejected proposals to lend directly to Main Street, including proposals for loans to state infrastructure banks, to Fannie Mae and Freddie Mac (two government supported entities that hold trillions of dollars in mortgages), to modify underwater mortgages, and to students to refinance their debts. Throughout, Fed officials have taken the view that they lack the legal authority for such lending and in particular, that federal law requires there be “good collateral” for any such loans.

However, such requirements did not stop the Federal Reserve from lending $29 billion to JPMorgan Chase to purchase Bear Stearns in March 2008, secured only by Bear Stearns’ shaky mortgage-related assets. This led Paul Volcker, a former Fed chairman, to express concern that the Fed’s intervention was testing the limits of its lawful powers and would call into question the Fed’s political independence if the central bank were viewed “as the rescuer or supporter of a particular section of the market,” such as mortgage-backed securities, collateralized debt obligations (CDOs), and other exotic financial instruments. Volcker warned that such allocation decisions are inherently political—“not strictly a monetary function in the way it’s been interpreted in the past”—and are more properly made by the elected branches of government as fiscal policy.

Yet, throughout 2008–2009, the Fed expanded its lending well beyond its traditional statutory authority, including to primary dealers in U.S. Treasury securities and foreign exchange swap lines for foreign central banks. The Fed effectively lent them more than a trillion U.S. dollars in exchange for a specified amount of their currencies until they were able to return those dollars for their currencies at the same exchange rate. The Fed also lent more than $700 billion to a facility of its own creation, a “special purpose entity,” to purchase commercial paper directly from major corporate borrowers, which helped prop up big businesses and cartels while ignoring the small and moderate-sized businesses and family enterprises that give life to Main Streets across the country. It was clear that the courts and political branches of government would not interfere with the Fed’s determination of what constitutes good collateral and the scope of its lawful powers in “unusual and exigent circumstances,” particularly when helping Wall Street in a crisis.

The Federal Reserve expanded its support for Wall Street in other unconventional ways that also suggested a bias in favor of the private financial interests that sit on the Fed’s own governing boards. In the fall of 2008, the Fed made an emergency equity investment in American International Group (AIG), taking a 79.9 percent interest in the global insurance conglomerate, all to make sure that AIG continued paying off on its credit default swaps (CDS) to Goldman Sachs and other counterparties. These swaps provided insurance against a downturn in the housing and mortgage markets. However, they also allowed Goldman Sachs and other speculators to bet against the same toxic mortgage-backed securities that they had created and already sold off to unsuspecting clients and investors. By rescuing AIG, an extraordinary measure that tested the limits of its authority, the Fed was no longer simply the lender of last resort: it was now the “buyer, dealer, and gambler of last resort,” serving as the gambling house to prop up the market for derivative contracts and to cover the wagers and losses of the global casino.

Goldman Sachs and other giant banks and hedge funds have engaged in similar shady and speculative activities abroad, for instance, betting on Greek, Spanish, and Italian sovereign and private debt. Through the use of derivatives, Goldman Sachs shorted the same Greek debt that it had previously helped the Greek government hide through other derivatives, namely currency swaps that allowed Greece to swap debt it had issued in dollars and yen for euros, using an outdated exchange rate that implied a reduction in debt. The European Central Bank (ECB) and International Monetary Fund (IMF) assured that these speculators would be paid off on their bets. Along with JPMorgan Chase and other big banks, Goldman Sachs would then take advantage of the austerity imposed on Greece and other countries by setting up infrastructure funds to buy up state-owned assets in fire sale privatizations.

Unlike the Federal Reserve’s lending programs, which have at least a semblance of statutory guidelines, the Fed has more discretion in its asset purchase programs, which have made a longer lasting effort at trickle-down monetary policy. In the first QE program, which began in November 2008, the Fed purchased $1.25 trillion in mortgage-backed securities, $300 billion in Treasury securities, and $200 billion in Fannie Mae and Freddie Mac “agency debt,” all with money newly created by the Fed. The Fed was no longer just taking distressed mortgage bonds as collateral on loans, which had been Volcker’s concern, it was now actually purchasing more than a trillion dollars in these assets.

When this QE program ended, the U.S. economy once again slowed. The financial markets had become addicted to the Fed’s massive bond purchases and when each QE ended, the markets needed another fix. The Fed responded in November 2010 with QE2 to purchase an additional $600 billion in Treasury securities. Next came “Operation Twist” a year later, in which the Fed shifted some of its portfolio of Treasury securities from short-term to long-term maturities, intended to bring down long-term interest rates on other securities and mortgage loans. Finally in September 2012, the Fed announced QE3, an open-ended pledge to purchase $40 billion of agency MBS and $45 billion of long-term Treasury securities each month. QE3 would last nearly two years.

Critics have charged the QE approach with pumping up financial markets, creating new bubbles, ignoring the needs of real people and Main Street businesses, and weakening the currencies of countries following the approach, thereby impairing growth in other nations. Yet, the Fed’s QE programs have become the model for other major central banks. Beginning in March 2009, the Bank of England purchased about $569 billion in assets, in at least three rounds, increasing the total each time the effect of the previous round wore off. As the Fed was tapering off its QE3 purchases, the Bank of Japan launched its own QE program of $1.4 trillion in asset purchases. More recently, the ECB announced its QE program of $69 billion a month in public and private bond purchases, to total more than $1.3 trillion.

Many central bankers were aware of the limited effectiveness of these QE programs, but supported them nonetheless in the absence of any ongoing fiscal stimulus. Although Ben Bernanke, the Fed chairman at the time, was calling on the government to do more on the fiscal policy side, extension of Bush’s tax cuts was the trickle-down approach he most favored and which was accepted by the Obama administration through 2012.

In helping Wall Street and global capital markets, the Fed has stretched its asset purchasing well beyond its traditional powers. Meanwhile, it has claimed a lack of authority to serve Main Street interests, even on a far lesser scale. For instance, there have been proposals for the Fed to purchase state and municipal bonds to help finance construction and repair of roads and bridges. The Fed presently lacks authority to purchase municipal bonds with maturities of more than six months, so Fed purchases of longer maturities would require congressional action. There have also been proposals for the Fed to pump money into state infrastructure banks, and to purchase student debt and to allow moratoriums on debt repayment while labor markets remain weak. Others have urged the Fed and the ECB to make cash transfers directly to consumers and taxpayers. From both sides of the spectrum came proposals for mortgage loan modifications, financed either directly by the Fed or by the Treasury with Fed support. These kinds of QEs for Main Street, like the Fed’s QEs for Wall Street, would incur no costs to government and would not add to deficits; quite the contrary, since they would put taxpaying resources back to work. Such monetary policies would have prodded the United States and the Eurozone away from austerity and in the direction of full employment.

Why help Wall Street creditors and not Main Street debtors? Why purchase trillions of dollars of mortgage-backed securities from banks, but not help the actual homeowners who are upside down on their mortgages? With the QE approach, central banks are picking winners and losers in the marketplace, which should raise concerns about both their social neutrality and their political independence. In criticizing the proposed Trans-Pacific Partnership (TPP) agreement, Senator Elizabeth Warren has noted that a rigged process inevitably leads to rigged outcomes. It is much the same with the Federal Reserve, which is captured by big banking interests and rigged by design. Not surprisingly, the Fed also fosters rigged outcomes.

Although the Federal Reserve claims that its allocation decisions are disinterested, a review of its governance structure may suggest otherwise. The public face of the Fed is the chairman of its Board of Governors in Washington, D.C. For nearly two decades that was Alan Greenspan, who came to the Fed through the “revolving door” from Wall Street, where he had been a director at JPMorgan. Ben Bernanke, formerly the chief economics advisor in the Bush White House, was Fed chairman from 2006–2014, during the peak of the financial crisis, and was also the architect of the Fed’s massive lending and asset purchase programs. Janet Yellen, who became Fed chair in 2014, was president of the Federal Reserve Bank of San Francisco during the bubble and embraced Bernanke’s QE strategies since first becoming the Fed’s vice chair in 2010. In addition to the Fed chairman and Board of Governors, the Fed’s Open Market Committee (FOMC) and the Federal Reserve Bank of New York (the NY Fed) make many of the key decisions that have helped Wall Street. This is not at all surprising since the FOMC consists of the seven-member Board of Governors along with the presidents of the twelve privately owned regional Federal Reserve banks. The regional Feds are governed by private boards of directors that are dominated both formally and in practice by the private commercial banks that own the shares in these banks. The Fed’s governance structure, like all “independent” central banks, is not all that independent of private financial interests. Rather, these central banks are captured agencies. The fox is running the henhouse.

The Obama administration’s main legislative response to the financial crisis was the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, which included a provision introduced by Senator Bernie Sanders requiring the U.S. Government Accountability Office (GAO) to conduct unprecedented audits of the Federal Reserve’s governance, monetary policy, and emergency lending programs during the crisis. These audits revealed Fed favoritism of big Wall Street interests with secret emergency loans, including massive support for many of the bankers who sit on the boards of the regional Fed banks. For instance, Jamie Dimon, the CEO of JPMorgan Chase, sat on the board of the NY Fed while his bank received an eighteen-month exemption from risk-based leverage and capital requirements, and $29 billion in financing to acquire Bear Stearns, while the Fed assumed Bear Stearns’ toxic assets, thereby relieving JPMorgan of huge liabilities in the future.

Another GAO audit found serious conflicts of interest in Federal Reserve governance. For instance, in 2008, Stephen Friedman, the chairman of the NY Fed, sat on the board of directors of Goldman Sachs and owned Goldman stock, while the NY Fed was approving Goldman’s application to become a bank holding company to obtain access to the Fed’s low-interest loans. This was also while Friedman chaired the search for a new president of the NY Fed that resulted in the selection of William Dudley, who had recently been a partner and managing director at Goldman and served for a decade as Goldman’s chief U.S. economist.

In September 2010 Reuters published a special investigative report of the Federal Reserve’s selective disclosure of sensitive information about monetary policy to its favored clientele in the private financial sector. Reuters found that private financial analysts and former Fed officials were profiting from their leaked information, possibly in violation of federal law. Moreover, these backroom exchanges appear to be among the many quid pro quos in a system of opaque subsidies and part of a larger problem of private financial influence over economic decision-making by the government. In 2011, the Fed announced certain restrictions on meetings with senior Fed officials. But it is difficult to change the Fed’s culture of revolving doors and cozy relations with private financial institutions. In May 2015, the Fed announced that the U.S. Justice Department was conducting a criminal investigation of a 2012 disclosure of confidential information about a crucial FOMC meeting to Medley Global Advisors, a firm that sells financial analysis to investors, is owned by the Financial Times, and is part of Pearson PLC, a huge multinational publishing and education conglomerate. House Republicans are also pressing for information about the leak and the Fed’s own internal inquiry.

Finally, the Fed’s conflicts of interest have raised questions about the rigor and impartiality of its regulatory supervision and oversight of the biggest banks. For instance, in 2009, the NY Fed commissioned a secret internal investigation of itself conducted by a Columbia University finance professor, which according to the Wall Street Journal, revealed “a culture of suppression and discouraged regulatory staffers from voicing worries about the banks they supervised.” The review recommended various reforms to encourage “critical dialogue and continuous questioning.” Yet, four years later the Fed’s culture was still in question when one of its former bank examiners, Carmen Segarra, filed a lawsuit alleging that the NY Fed had interfered with her oversight of Goldman Sachs. Segarra’s allegations could not be easily ignored since she had secretly recorded audio of some forty-six hours of meetings and conversations with her colleagues and superiors.

The Fed’s governance and independence are often defended by arguments that its current methods help to draw on the expertise of bankers and financiers. But the exclusion of all social groups other than bankers from Fed governance skews the institution’s decision-making. Reforming central bank governance to include a diversity of perspectives and interests could prod the institution into once again supporting public infrastructure and a jobs program.

It would also be worthwhile to break the monopoly of central banks in the issuance of currency by funding some government operations with money created and issued by treasuries and finance ministries—money that would not add a penny to public debt. This is what President Abraham Lincoln did by issuing more than $400 million in U.S. notes, the so-called Greenback, to pay the huge costs of the American Civil War and national economic development programs. A century earlier, colonial Pennsylvania enjoyed fifty-two years of non-inflationary growth by issuing and lending its own currency into circulation, thereby financing major development of infrastructure without incurring debt or high tax burdens. Adam Smith, in his classic work Wealth of Nations (1776), praised Pennsylvania’s success with government-issued money. Such proposals have been introduced in Congress over the years, but Wall Street lobbying has prevented such legislation from passing.

In the United States and elsewhere, the model of central bank independence is built on sand, propped up with trillions of dollars in market interventions designed and implemented by captured central banks. This central bank exception to democracy is not sustainable. It undermines broad-based economic well-being by concentrating power—and therefore wealth and income—in fewer and fewer hands. Any real progressive reform will require making the governing boards and policy-making committees of central banks genuinely inclusive to reflect a wider range of interests and to facilitate a wider discussion on the formulation of monetary policy. The longer reform is delayed, the longer we will have to live with huge redistributions of wealth and income from the many to the few, from Main Street to Wall Street.

Timothy A. Canova is a professor of law and public finance at Nova Southeastern University’s Shepard Broad College of Law in Fort Lauderdale, Florida. An earlier version of this article was published in Limes, the Italian journal of geopolitics, in February 2015 in a special volume, Money and Empire (Moneta e Impero).